Based on the link (https://www.youtube.com/shorts/vPVu7iGn6Sk) we can see that the prosecutor deemed that Nadiem has an income of IDR 5,2 trillion from amount that reported on Nadiem personal income tax return (PITR). Nadiem defended that the tax reported on his PITR is not based on income but based on the Gojek share’s that conducted an initial public offering (IPO).

An IPO is a strategic move by a company to raise additional capital from investors by listing the company on the Indonesia Stock Exchange (IDX). The Directorate General of Taxes (DJP), as the Indonesian tax authority, has issued Ministry of Finance regulation number 282/KMK.04/1997 as lastly changes with the Minister of Finance regulation number 81 of 2024, which stipulates that founding shareholders are subject to an additional final tax of 0.5% of the share value at the time of the IPO. This final tax is levied when the shares begin trading on the stock exchange and is not affected by any subsequent sale of the founding shareholders’ shares. If the founding shareholders also sell these shares, there will be two instances of final tax being levied: a final income tax on share transactions on the Indonesia Stock Exchange amounting to 0.1% of the transaction value, and an additional 0.5% on the founding shareholders’ shares. Founding shares are shares held by the company’s founders at the time of the IPO. Founding shares include:

- Shares resulting from the capitalization of share premium issued after the IPO.

- Shares resulting from a stock split of the founder’s shares.

Article 247 of The Minister of Finance regulation No. 81 of 2024 defines a founder as an individual or entity whose name is recorded in the list of shareholders of a limited liability company prior to the registration statement submitted to the financial services authority in connection with the initial public offering becoming effective.

An additional tax of 0.5% is applied to founding shareholders and becomes payable when the company’s shares are traded on the stock exchange; it is collected by the issuer no later than one month after the additional income tax becomes payable, and the issuer issues and delivers proof of collection to the founding shareholders.

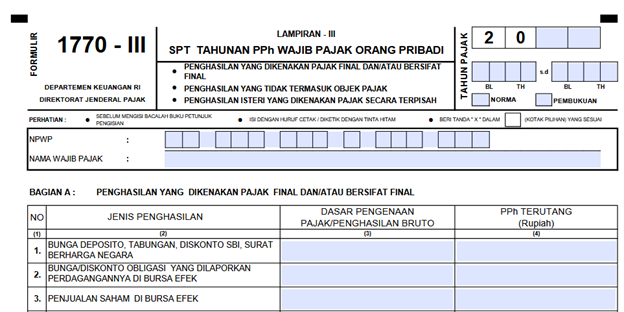

This additional taxation on founder shares at the time of the IPO means that the company’s founding shareholders should by recognize the income tax subject to final income tax on share transactions and enter it in form 1770 attachment III in section A.3.

Even though, in practice, it does not increase the wealth of the founding shareholders but is an expense. Under these provisions, an IPO entails an additional tax liability of 0.5% for founder shareholders, regardless of any share sale transactions.

By Tommy HO – Managing Partner

TBrights is a tax consultant in Indonesia that is currently an Integrated Business Service in Indonesia that can provide comprehensive tax and business services.

Referance:

- The Minister of Finance Regulation No. 81 of 2024 on Tax Provisions in Connection with the Implementation of the Core Tax Administration System.